Project loan and project finance in India – business consultant guidance

A project loan is when we are starting a business whether it is manufacturing, trading, supply, or any other kind of business project — the financial requirement to fulfill all the capital needs is called a Project Loan.

First, we measure the total costing of the business and prepare the DPR (Detailed Project Report). In the DPR, we include the cost of everything related to our project, which is called the project cost. For the business you are starting, you also need working capital to run it.

Formula

Total Term Loan + Cash Credit Limit = Project Loan

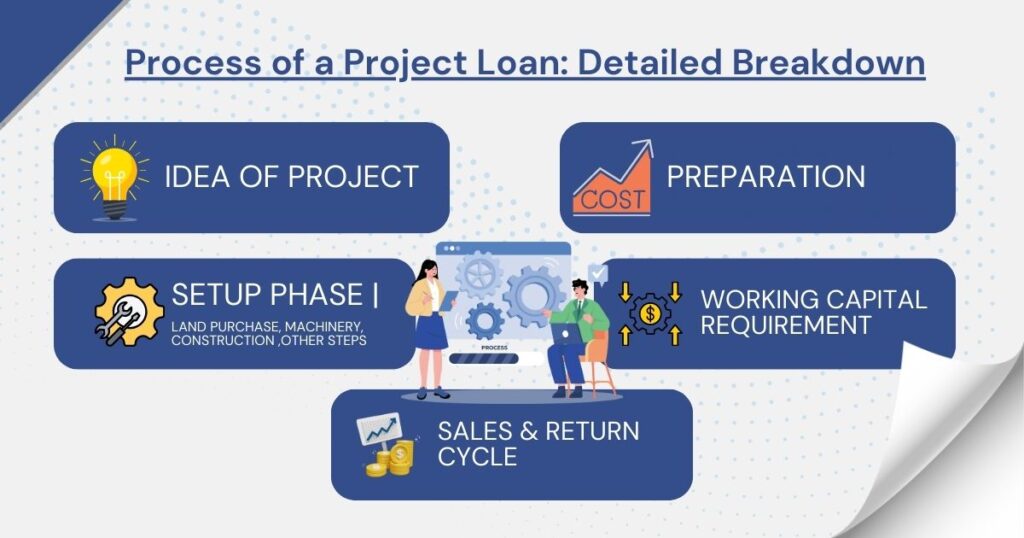

For example, if we have a business project in mind, we might purchase land, install machines, do construction, and take other important steps. Then, when the entire setup process of the business is completed, we need working capital to operate the business. This is given as a CC (Cash Credit) limit.

Key Uses for Project Loans

Project loans support businesses in different sectors, especially where initial investments are high. Typical areas include:

- Manufacturing units (e.g., furniture factories, textile mills)

- Trading businesses

- Supply and distribution chains

- Food processing and packaging plants

- Retail and wholesale shops with expansion plans

Project loans typically consist of two main parts:

- Term Loan: For buying equipment, machinery, construction, or renovations.

- Working Capital (CC Limit): Funds for daily business activities—purchasing raw materials, paying staff, managing inventory.

This all-in-one approach helps ensure your business can move from blueprint to operation smoothly.

Process of a Project Loan: Detailed Breakdown

When you apply for a project loan, banks want to know exactly how much money you need and why. That’s why it’s vital to prepare a Detailed Project Report (DPR) and understand the different components of your project cost.

First, we decide the cost, and when our project is ready, we move toward sales. After the sales, the returns we get have a cycle period before they come back to us.

Elements of Total Project Cost

Here’s what usually goes into calculating the project cost:

- Land Acquisition Cost: Price for purchasing or leasing land.

- Machinery Cost: Investments in machines, equipment, and tools.

- Construction Cost: Building factories, offices, or warehouses.

- Working Capital: Funds for ongoing expenses (stocks, utilities, payroll).

The project cycle period (or cycling period) is the time between purchasing raw material and receiving payment from customers after your products are sold. This cycle is key to understanding how much working capital you’ll need.

It’s crucial to get your costing right. Banks assess every aspect of your plan. Inaccurate estimates can lead to funding issues or even loan rejections.

Role of the Detailed Project Report (DPR)

The DPR acts like your business blueprint. It includes:

- Detailed cost analysis

- Market research and demand forecast

- Resource requirements (raw materials, labor, utilities)

- Projected cash flows and profitability

Accurate and transparent reporting in your DPR boosts your credibility with banks and increases your chances of approval.

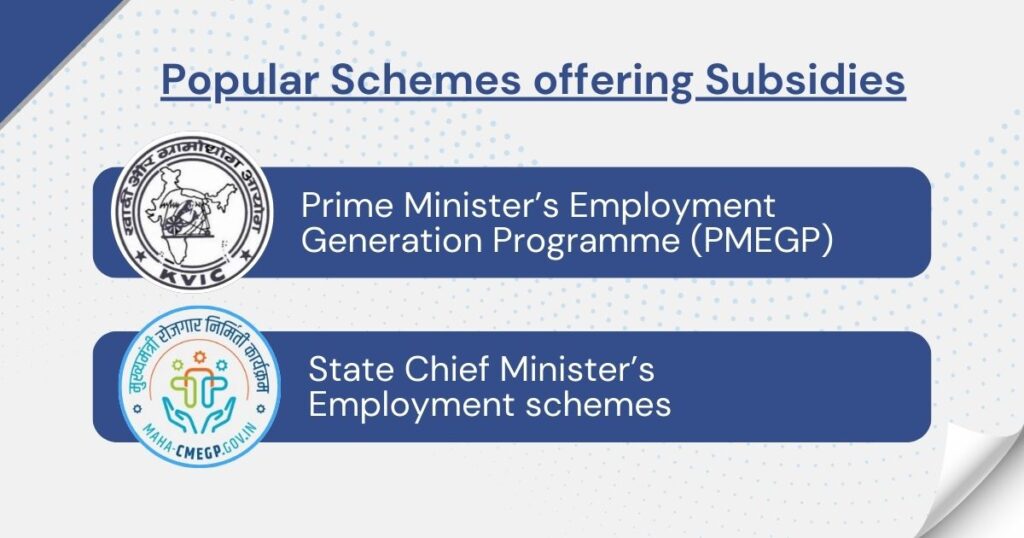

Government Subsidies and Bank Policies on Project Loans

Government initiatives in India make it easier for small businesses to get started or expand through project loans.

Popular Schemes offering Subsidies

- Prime Minister’s Employment Generation Programme (PMEGP)

- State Chief Minister’s Employment schemes

These schemes provide interest subsidies and partial funding support. For example, after the loan is sanctioned, a portion of the project cost might be reimbursed as a subsidy, or you could get a reduced interest rate for a specific period.

Bank Margin Requirements and Collateral

Different banks set different requirements for project loans:

- Some ask you to contribute 25% of the total cost (your own funds), others may require 30% or even 50%.

- Some banks need additional collateral security (like property or other assets).

- The exact margin and collateral depends on the bank’s policy and the nature of your business.

Benefits of subsidies:

- Reduce your financial burden

- Lower monthly outgoings

- Speed up return on investment

Understanding these can help you choose a scheme or bank that matches your needs.

“Watch this video guide on Project Loan explained in detail 👇”

Documentation Required for Project Loan Application

Once your documents are ready, here’s how to navigate a typical loan application:

Documentation for Proprietorship Firms

- PAN Card and Aadhaar Card of the owner

- Mobile Number and Email ID for OTP verification and correspondence

- MSME (Udyam) Registration

- GST Registration

- Bank Details (passbook, account statement)

- Land ownership documents for the land on which the project is set up (primary security is often required)

- Proof of address (utility bills or similar)

- Industry-related approvals, depending on the project:

- Pollution certificates (if applicable)

- Industrial area map/approval

- Fire safety clearances

- Import Export Code (IEC), if relevant

- Detailed Project Report (DPR)

- Passport-size photographs

Owning the land on which the business stands can simplify the approval process by serving as collateral.

Documentation for Other Constitutions

(These requirements vary by type; future blog posts and videos will cover each in detail.)

Registrations and Approvals You May Need:

- Certificate of incorporation or equal (for companies)

- Partnership deed (for partnership firms)

- Board resolution, Memorandum of Association, Articles of Association (for companies)

- KYC documents for all directors/partners

- Proof of business address

- Authorization letters for loan processing

The process is more involved for companies and LLPs, but the potential for raising higher funds is better.

Step-by-Step Process to Apply for a Project Loan in Banks

Once your documents are ready, here’s how to navigate a typical loan application:

- Fill out the bank’s project loan application form completely and accurately.

- Attach all required KYC documents (PAN, Aadhaar, business registrations, land and industry approvals).

- Submit your DPR along with the application.

- The bank reviews your credit history and civil score (equivalent to CIBIL/Credit Score).

- A score above 680-700 is generally needed for project loan approval. Lower scores or bad credit history can torpedo your application.

- Civil Score tracks past loans, repayments, and defaults.

- SMA (Special Mention Account) and NPA (Non-Performing Asset) refer to missed or delayed payments. Accounts with these tags raise red flags.

- The bank may discuss your project and hold a one-time meeting to clarify details.

- The application is processed over 7-15 working days, depending on workload and completeness of documents.

- The bank determines the margin (your contribution) and deducts it from the total project cost.

- Verification visit: A bank representative may visit your project site, factory, or office.

- Final sanction: Once all checks are complete, the loan amount is credited to your account.

- Subsidy application: If eligible, you submit required forms to DIC office or relevant departments for subsidy benefits.

Use this process as a checklist—missing steps hold up approvals.

Approval Timeframe: Most project loans finalize within 8 to 15 working days if your paperwork is in order.

Overview of Bank Charges and Post-Loan Process

Getting the loan is only half the journey. After disbursal, certain rules and responsibilities must be followed.

Typical Bank Charges

- Processing fees determined by Reserve Bank of India guidelines

- Legal and documentation charges (one-time)

- Periodic account maintenance charges

After-Loan Responsibilities

- Make timely EMI payments to maintain a good credit score

- Comply with bank’s reporting requirements (project updates, utilization certificates)

- Use government subsidies as per guidelines

- Don’t default—defaulting turns your account into NPA, hurting future eligibility

Key responsibility: Always make your monthly payments on time and keep records updated.

Future Topics: Documentation and Processes for Other Business Constitutions

While this post focused on proprietorship firms, the application process for companies, LLPs, and partnership firms is a bit different.

Upcoming posts will cover:

- Private Limited Company loan documentation

- LLP and Partnership Firm project loan process

- Changes in compliance for each structure

For the latest updates and expert advice, follow this blog and subscribe to the Beginquest Services YouTube channel.

Conclusion

A project loan can transform a well-crafted business plan into a profitable venture. Setting up your documentation and understanding the process are key steps. Subsidies and proper constitution selection can make your journey smoother and more sustainable.

If you run a business in Lucknow or nearby, consider reaching out to a trusted business consultant in Lucknow who can help you with every step—from forming your company to claiming your subsidies.

Take the next step confidently for your venture. The right project loan is your gateway to building something great!